Insurance plays an important role in financial planning. However, many people confuse life insurance and health insurance, thinking they serve the same purpose. In reality, they are designed to protect against very different risks.

If you are searching for “life insurance vs health insurance,” you likely want to understand which one you need, how they differ, and whether you should have both. Life insurance protects your family financially after your death. Health insurance helps pay medical expenses while you are alive.

Both policies offer financial protection, but they cover different life events. Choosing the right coverage depends on your age, health, family responsibilities, and financial goals.

This detailed guide explains life insurance vs health insurance in simple terms. You will find comparison tables, clear definitions, real-life examples, advantages and disadvantages, and frequently asked questions. The goal is to help you understand how each policy works so you can make informed decisions.

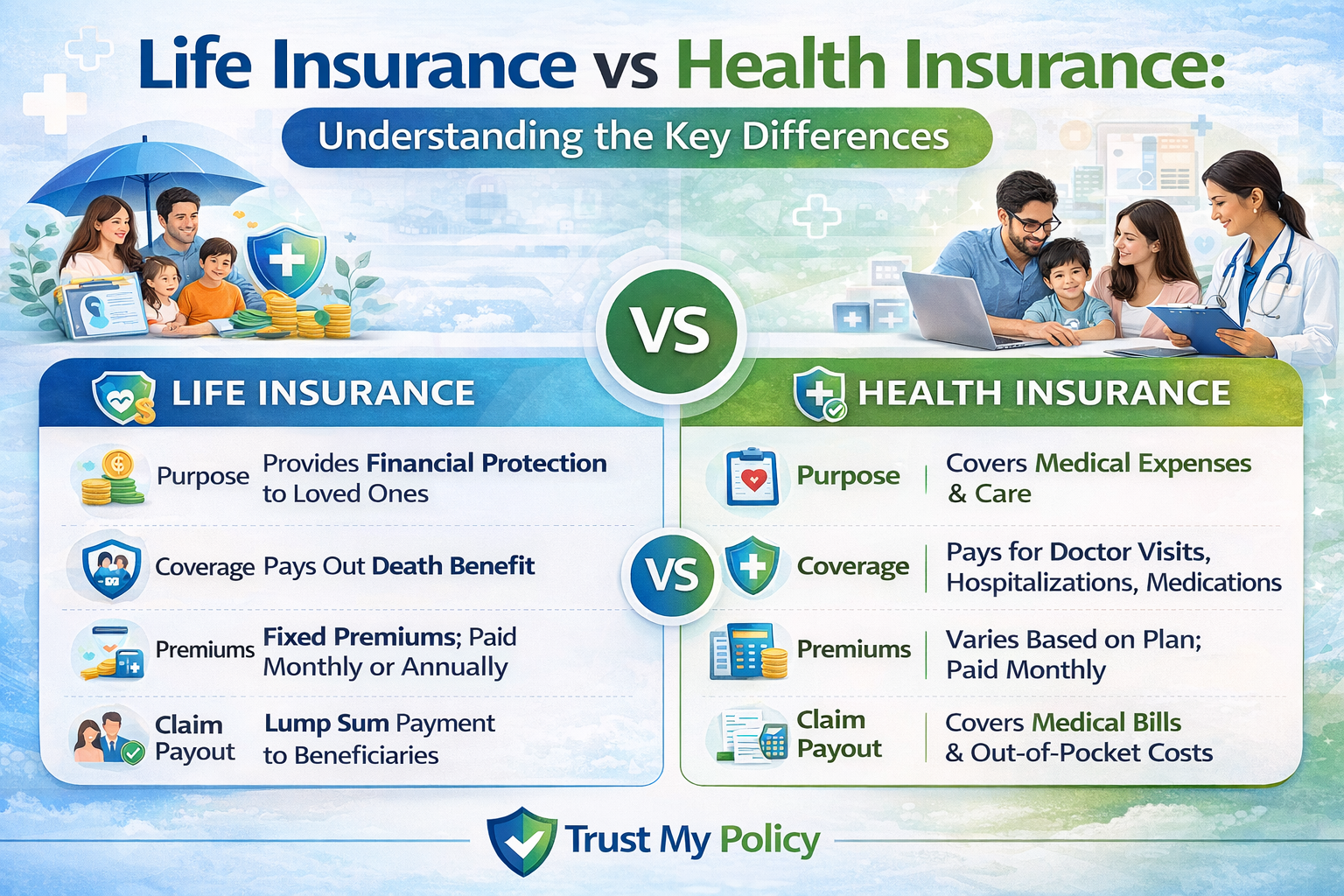

Life Insurance vs Health Insurance

| Feature | Life Insurance | Health Insurance |

|---|---|---|

| Purpose | Provides financial support after death | Pays medical expenses during life |

| Who Receives Benefit | Beneficiaries (family members) | Policyholder or healthcare provider |

| Covers Medical Bills | No | Yes |

| Covers Death Benefit | Yes | No |

| Premium Payment | Monthly or yearly | Monthly or yearly |

| Claim Trigger | Death of insured person | Hospitalization or medical treatment |

| Long-Term Financial Planning | Yes | Yes |

| Legal Requirement | Usually optional | Mandatory in some countries |

What Is Life Insurance?

Life insurance is a contract between you and an insurance company. You pay regular premiums, and in return, the insurer pays a lump sum amount (called a death benefit) to your chosen beneficiaries if you pass away during the policy term.

The purpose of life insurance is to provide financial security to your family or dependents.

Types of Life Insurance

-

Term Life Insurance

-

Covers a specific period (10, 20, 30 years)

-

Pays benefit only if death occurs during the term

-

Usually lower premium

-

-

Whole Life Insurance

-

Covers entire lifetime

-

May include savings or investment component

-

Higher premium

-

What Life Insurance Covers

-

Income replacement

-

Funeral expenses

-

Outstanding debts

-

Education expenses for children

-

Mortgage payments

Life insurance does not cover medical expenses or routine healthcare costs.

What Is Health Insurance?

Health insurance is a policy that helps pay for medical expenses such as hospital stays, doctor visits, surgeries, and prescription drugs.

The purpose of health insurance is to reduce the financial burden of medical treatment.

What Health Insurance Covers

-

Hospitalization

-

Doctor consultations

-

Surgeries

-

Diagnostic tests

-

Emergency care

-

Prescription medication (depending on plan)

Health insurance does not provide a payout after death.

Common Health Insurance Features

-

Deductibles

-

Copayments

-

Coinsurance

-

Network hospitals

-

Annual coverage limits

Health insurance protects you while you are alive.

Detailed Comparison Table: Life Insurance vs Health Insurance

| Criteria | Life Insurance | Health Insurance |

|---|---|---|

| Main Objective | Financial support after death | Cover medical costs |

| Benefit Type | Lump sum payout | Reimbursement or direct payment |

| Who Benefits | Family members | Policyholder |

| Covers Hospital Bills | No | Yes |

| Covers Critical Illness | No (unless rider added) | Yes (depending on plan) |

| Claim Condition | Death of insured | Medical treatment needed |

| Policy Duration | Fixed term or lifetime | Usually annual renewal |

| Investment Component | Sometimes (whole life) | Usually none |

| Mandatory in Some Countries | Rarely | Yes in certain regions |

| Suitable For | Breadwinners, parents | Everyone |

How Life Insurance Works

-

You choose coverage amount.

-

You pay premiums regularly.

-

If you pass away during coverage period:

-

Beneficiaries file claim.

-

Insurer pays agreed amount.

-

If you survive the term (for term life):

-

No payout.

-

Policy expires.

Life insurance focuses on financial protection for dependents.

How Health Insurance Works

-

You select a health plan.

-

You pay monthly or annual premiums.

-

When you need medical treatment:

-

You pay deductible or copay.

-

Insurer pays remaining covered amount.

-

Health insurance reduces immediate healthcare costs.

Pros and Cons of Life Insurance

Advantages

-

Provides financial security to family

-

Covers major debts

-

Helps in long-term planning

-

Peace of mind for dependents

Disadvantages

-

No benefit if policy expires (term plans)

-

Does not cover medical expenses

-

Premiums increase with age

Pros and Cons of Health Insurance

Advantages

-

Reduces hospital expenses

-

Covers emergency treatment

-

Protects savings

-

Encourages regular medical care

Disadvantages

-

Does not provide death benefit

-

May include deductibles and copays

-

Annual premium increases possible

Real-Life Use Cases

Example 1: Family Breadwinner

A 35-year-old parent with two children buys life insurance worth $500,000.

If the parent dies unexpectedly:

-

Family receives lump sum.

-

Funds can cover education and living expenses.

Health insurance alone would not provide this financial support.

Example 2: Medical Emergency

A 40-year-old individual requires surgery costing $20,000.

With health insurance:

-

Insurer covers most of the expense.

-

Policyholder pays deductible.

Life insurance would not help with this medical cost.

Example 3: Single Individual

A young professional without dependents may prioritize health insurance first, as it protects against immediate medical risks.

Example 4: Married Couple with Mortgage

They may need:

-

Life insurance to protect family if one partner dies.

-

Health insurance to cover medical treatments.

Both policies serve different but important purposes.

Common Mistakes and Misunderstandings

1. Thinking Life Insurance Covers Medical Bills

It does not cover healthcare costs unless specific riders are added.

2. Believing Health Insurance Protects Family After Death

Health insurance does not provide a death payout.

3. Choosing Only One Without Assessing Needs

Some individuals need both types of insurance.

4. Ignoring Long-Term Planning

Life insurance is part of estate planning and income protection.

5. Delaying Purchase

Premiums increase with age and health risks.

Do You Need Both?

In many cases, yes.

Consider Life Insurance If:

-

You have dependents

-

You have debts

-

You are primary earner

-

You want financial legacy planning

Consider Health Insurance If:

-

You want protection against medical expenses

-

Healthcare costs are high in your country

-

You lack employer-sponsored coverage

They serve different roles and often complement each other.

Frequently Asked Questions (FAQs)

1. Which is more important: life insurance or health insurance?

It depends on your situation. Health insurance protects you during life. Life insurance protects your family after death.

2. Can I have both life and health insurance?

Yes. Many people carry both for complete financial protection.

3. Does life insurance cover critical illness?

Not usually, unless a critical illness rider is added.

4. Does health insurance pay after death?

No. Health insurance only covers medical expenses while alive.

5. Is life insurance mandatory?

Generally no, but health insurance may be required in some countries.

6. Which is cheaper?

Health insurance costs vary by medical coverage. Term life insurance is often affordable for young, healthy individuals.

7. Can seniors buy both policies?

Yes, but premiums increase with age and health condition.

Key Differences at a Glance

-

Life insurance protects dependents after death.

-

Health insurance covers medical expenses during life.

-

Life insurance pays beneficiaries.

-

Health insurance pays hospitals or policyholders.

-

Both are part of financial risk management.

Conclusion

Understanding life insurance vs health insurance is essential for smart financial planning. These two policies serve different purposes and address different risks.

Life insurance ensures your loved ones are financially secure if you are no longer there. Health insurance protects you from high medical costs during your lifetime.

Choosing between them depends on your responsibilities, health, and financial goals. In many cases, having both provides balanced protection.

Carefully review your needs and long-term plans before deciding. Proper insurance planning can help protect both your present and your family’s future.

Disclaimer: This article is for educational purposes only. Trust My Policy is an independent informational platform and does not sell insurance products or represent any insurance provider. Readers should consult official policy documents or licensed professionals for personalized advice.