Life Insurance vs Health Insurance: Complete 2026 Guide

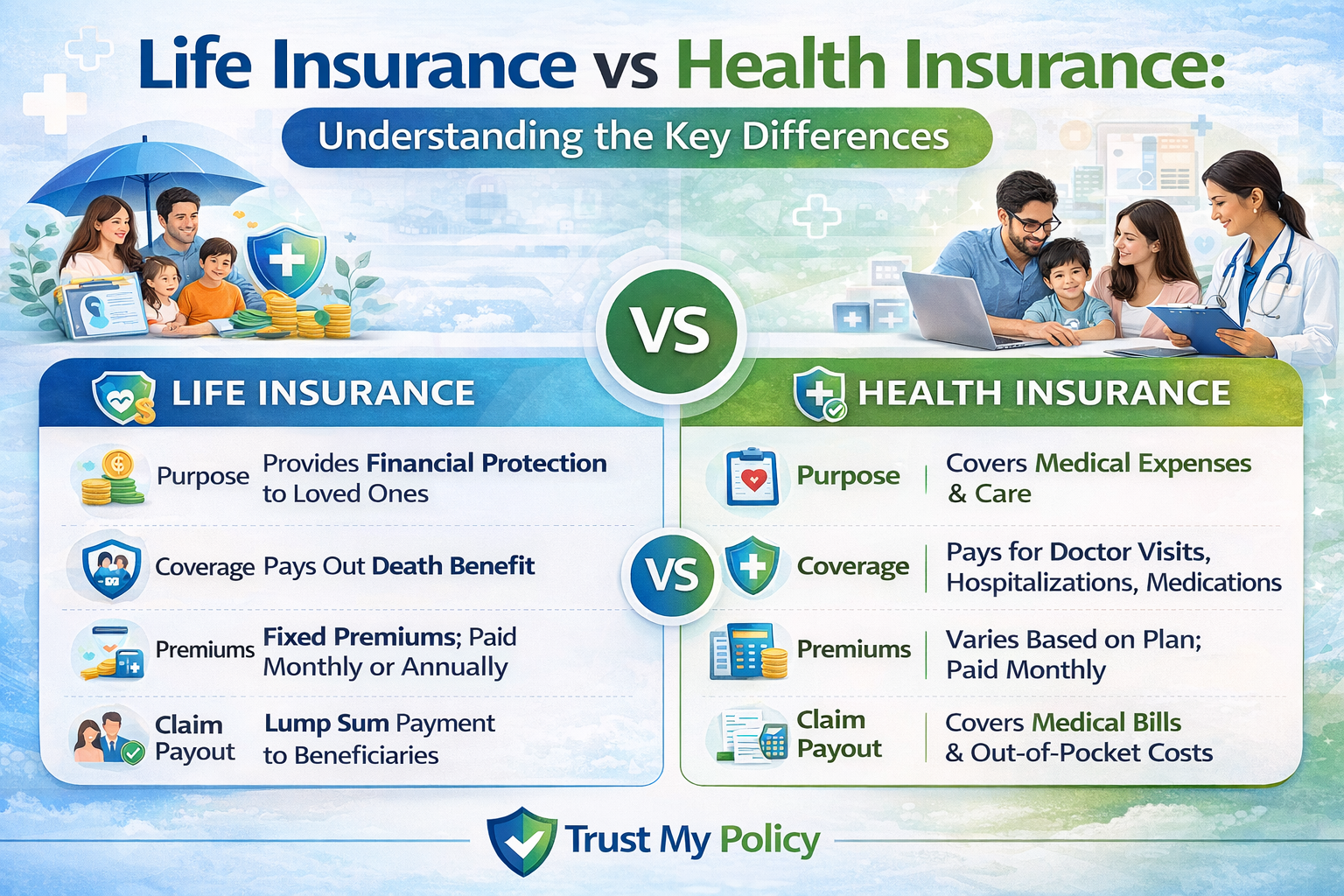

Health insurance pays for medical treatment while you are alive — doctor visits, hospital stays, prescriptions, and surgery. Life insurance pays a lump sum to your beneficiaries when you die. They serve completely different purposes and address completely different risks. In 2026, health insurance averages $752/month for a 40-year-old on an ACA Silver plan (Venteur 2026). Term life insurance for the same person averages $55/month for $500,000 coverage over 20 years (MoneyGeek 2026). Most working adults with dependants need both.

Introduction

When Ravi, a 33-year-old software engineer from Seattle, got his first full-time job offer, he had to fill out two separate insurance forms on the same day — one for health insurance, one for life insurance. He had no idea they were fundamentally different products. “Is life insurance just in case I get really sick?” he asked his HR team. No: health insurance pays your medical bills while you are alive; life insurance pays your family when you die. They serve completely different purposes and most working adults need both — often at the same time.

Life insurance vs health insurance in 2026 is a comparison that reveals two entirely different financial tools often confused because both have “insurance” in the name. According to MoneyGeek 2026 analysis, a 40-year-old can get $500,000 of 20-year term life insurance for $55/month — affordable protection for a family’s financial future. Health insurance for the same person averages $752/month on a Silver ACA plan. The costs are dramatically different because they solve different problems: one protects your income-earning future, the other protects your body today.

In this guide you will learn exactly what life insurance and health insurance cover and exclude, why you almost certainly need both, how much each type costs in 2026 for different age and health profiles, four real-life scenarios showing when each matters most, and the biggest mistakes people make when prioritising one over the other.

Quick Summary: Life Insurance vs Health Insurance

| Feature | Health Insurance | Life Insurance |

| When it pays | While you are alive — covers medical costs | When you die — pays a lump sum to beneficiaries |

| What it covers | Doctor visits, hospital, prescriptions, surgery | Mortgage, income replacement, debts, family living costs |

| Who benefits | You (the policyholder) | Your family / named beneficiaries |

| Is it required? | ACA-compliant plans required by most employers | Never legally required — but financially essential with dependants |

| Average monthly cost 2026 | $752/month Silver ACA plan, age 40 (Venteur 2026) | $55/month term life $500k 20yr, age 40 (MoneyGeek 2026) |

| Has a deductible? | Yes — $0–$7,000+ | No deductible — full death benefit paid |

| Coverage period | Annual — renews each year | Term (10–30 years) or permanent (whole life) |

| Regulated by | CMS, state DOI (US); FCA (UK) | State DOI (US); FCA (UK) |

What Is Health Insurance?

Health insurance is a contract between you and an insurer to share the cost of your medical care. You pay a monthly premium to keep the policy active. When you use healthcare — seeing a doctor, filling a prescription, having surgery, or staying in hospital — your health plan pays a portion of the cost after your deductible and copays are met.

Think of health insurance as a maintenance plan for your body. It covers you while you are alive and using the healthcare system. Without it, a single hospitalisation in the US can cost $15,000–$50,000+. A serious illness like cancer can generate $300,000+ in treatment costs. Health insurance converts that catastrophic financial risk into predictable monthly payments with a capped out-of-pocket maximum ($9,450 individual in 2026 per CMS).

Health insurance is used regularly — routine checkups, prescriptions, specialist visits — and covers short-term and long-term medical needs throughout your lifetime. It is the most actively-used insurance most people carry.

For a complete breakdown of health insurance costs by plan type and metal tier, see our guide on [INTERNAL LINK: how health insurance works in 2026 — premium deductible copay and OOP maximum explained]

What Is Life Insurance?

Life insurance is a contract that pays a specified sum — the death benefit — to your named beneficiaries when you die. You pay premiums to keep the policy active. The insurer pays the death benefit regardless of the cause of death (within policy terms and exclusion periods). Life insurance does not pay for medical treatment. It does not cover illness costs. It does not help you while you are alive.

Think of life insurance as a financial safety net for the people who depend on you. If you die tomorrow, would your partner be able to pay the mortgage? Would your children’s education be funded? Would your family cover their living costs without your income? Life insurance answers all three questions with a single lump sum payment.

There are two main types. Term life insurance covers you for a fixed period (10, 20, or 30 years) and pays the death benefit only if you die within that term. It is the most affordable type. Whole life insurance covers you for your entire lifetime and includes a cash value component that grows over time. It costs significantly more — according to MoneyGeek 2026, a 40-year-old pays $55/month for $500,000 term life vs $667/month for $500,000 whole life.

For a full comparison of term life vs whole life insurance, see our guide on [INTERNAL LINK: term life insurance vs whole life insurance — which is right for you in 2026]

How Life Insurance and Health Insurance Work: Side by Side

- You Experience a Medical Emergency — Health insurance: covers hospitalisation, treatment, and prescriptions after deductible and copays. Life insurance: pays nothing — you are still alive and health insurance handles medical costs.

- You Are Diagnosed With a Long-Term Illness — Health insurance: covers ongoing treatment, specialist visits, medications, and therapies. Life insurance: pays nothing while you are alive (though some policies with terminal illness riders pay a portion early if you have less than 12–24 months to live).

- You Die — Health insurance: immediately cancelled; pays nothing to your family. Life insurance: pays the full death benefit to your named beneficiaries tax-free, typically within 30–60 days of a valid claim.

- Your Family Needs Income Replacement — Health insurance: not applicable — it covers medical costs, not income. Life insurance: the death benefit replaces your income, enabling your family to pay the mortgage, fund education, and maintain their standard of living.

- You Need Both Simultaneously — A parent with a serious illness needs health insurance to pay for treatment AND life insurance to protect their family if they do not survive. These are complementary products. One does not substitute for the other.

Life Insurance vs Health Insurance: Detailed Comparison

| Criteria | Health Insurance | Life Insurance |

| Primary purpose | Pay for medical treatment while alive | Replace income and protect family after death |

| Benefit recipient | You (the patient) | Your beneficiaries (family, named individuals) |

| When benefit is paid | Each time you use healthcare (ongoing) | Once — when you die (lump sum) |

| Average cost age 30 (2026) | $320–$480/month Silver ACA | $18–$25/month term life $500k (NerdWallet 2026) |

| Average cost age 40 (2026) | $752/month Silver ACA (Venteur 2026) | $55/month term life $500k (MoneyGeek 2026) |

| Average cost age 50 (2026) | $950–$1,200/month Silver ACA | $120–$160/month term life $500k |

| Has a deductible? | Yes ($0–$7,000+) | No — full benefit paid |

| Tax treatment | Employer premium: pre-tax. ACA subsidy: tax credit | Death benefit: tax-free to beneficiaries. Premiums: not tax-deductible (personal) |

| Required by law? | Not legally required but ACA mandates coverage standards | Never legally required |

| Renews? | Annually — can change plans at open enrollment | Fixed term (term life) or permanent (whole/universal life) |

Most working adults with dependants need both products simultaneously. Health insurance handles today’s medical costs. Life insurance handles tomorrow’s family financial security. Neither replaces the other.

Real-Life Scenarios: When Each Insurance Type Saves You

Scenario 1: Ravi, 33, Software Engineer — Just Starting Out

Ravi is single with no dependants. His employer provides health insurance at $210/month (employee contribution). He has no life insurance and no one depends on his income. Health insurance: essential — one uninsured ER visit could cost $15,000. Life insurance: optional for now — no one depends on his income. His financial priority: max out employer health plan, build emergency savings. Verdict: Prioritise health insurance. Life insurance becomes essential when he marries or has children.

Scenario 2: Daniel, 36, Accountant — Young Family, $800,000 Mortgage

Daniel has a wife, one-year-old baby, and an $800,000 mortgage. His wife is on maternity leave. If Daniel dies, his family loses his $95,000 salary and cannot service the mortgage. Health insurance: $340/month (employer plan). Life insurance: $28/month for $1,000,000 30-year term. Combined cost: $368/month. Without life insurance, one accident leaves his family homeless. Verdict: Both are non-negotiable. The $28/month term life is the most cost-effective financial protection his family has.

Scenario 3: Linda, 58, Self-Employed — Pre-Medicare

Linda is 7 years from Medicare eligibility. She has two adult children who are financially independent. Health insurance: $1,150/month ACA Silver plan (her biggest financial concern). Life insurance: $240/month for $500,000 20-year term (she has an existing mortgage). Her adult children do not depend on her income — life insurance is less critical. Her $1,150 health insurance premium is her #1 financial risk. Verdict: Health insurance is the priority. She should review whether her life insurance is still necessary or whether critical illness insurance would serve her better at this life stage.

Scenario 4: The Ahmed Family — Both Essential Simultaneously

Ahmed (44) is diagnosed with stage 2 colon cancer. He has two children (ages 10 and 14) and a $450,000 mortgage. Health insurance: covers $280,000 in treatment costs — surgery, chemotherapy, radiation — with $9,450 OOP max paid. Life insurance: $500,000 20-year term. If Ahmed does not survive, his family receives $500,000 — enough to clear the mortgage and fund his children’s education. Both policies are paying simultaneously — health insurance funds his treatment; life insurance secures his family’s future. Verdict: This scenario shows exactly why both are needed at the same time. Neither can replace the other.

Pros and Cons: Life Insurance vs Health Insurance

| Pros of Health Insurance | Cons of Health Insurance | Pros of Life Insurance | Cons of Life Insurance |

| Covers medical costs throughout your life — essential for financial survival | Monthly premium is the highest insurance cost for most adults ($320–$1,200+) | Provides large lump sum to family at very low cost — term life $55/month buys $500k coverage | Pays nothing while you are alive — does not help with medical bills |

| Caps catastrophic medical costs at $9,450 OOP max per year (CMS 2026) | Premiums rise annually — ACA Silver plan for a 50-year-old averages $950–$1,200/month | Death benefit is tax-free to beneficiaries under US federal law | Term life expires — if you outlive the term, premiums are sunk cost with no payout |

| Preventive care is free — ACA-mandated checkups, screenings, vaccinations | High deductible plans require $1,700–$7,000 before major coverage begins | Replaces income — one policy can fund mortgage, education, and family living costs | Whole life is expensive — $667/month for same $500k coverage that costs $55/month on term (MoneyGeek 2026) |

| Covers prescription drugs — essential for chronic condition management | Coverage gaps — dental, vision, and long-term care often excluded | Peace of mind — family is financially protected regardless of cause of death | Requires medical underwriting — pre-existing conditions increase premiums or result in exclusions |

| Employer plans are pre-tax and often employer-subsidised | Changing jobs can disrupt coverage — COBRA is expensive ($500–$700/month) | Can be used for business protection — key person insurance, partnership buy-sell agreements | Life insurance premiums are not tax-deductible for individuals (unlike business use) |

5 Common Mistakes When Comparing Life Insurance and Health Insurance

Mistake 1: Assuming Life Insurance Covers Medical Bills

Why it happens: Both have “insurance” in the name. What to do instead: Remember the rule — health insurance pays while you are alive; life insurance pays when you die. They solve entirely different problems. You cannot substitute one for the other.

Mistake 2: Prioritising Life Insurance Over Health Insurance When Young and Single

Why it happens: Life insurance salespeople are aggressive. Young singles with no dependants are targeted. What to do instead: If you have no dependants and no one relies on your income, health insurance is far more immediately critical. One uninsured hospital stay can cost $20,000–$50,000. Life insurance is essential only when others depend on your income.

Mistake 3: Dropping Life Insurance When the Mortgage Is Paid Off

Why it happens: People think the mortgage was the only reason for life insurance. What to do instead: Reassess. If your spouse depends on your income (even in retirement), or you have outstanding debts, or your estate will owe taxes — life insurance may still be valuable even without a mortgage. Speak to a financial adviser before cancelling.

Mistake 4: Buying Whole Life Insurance Instead of Term + Investing the Difference

Why it happens: Whole life policies are heavily sold and generate large commissions. What to do instead: For most people, $55/month term life + $612/month invested beats $667/month whole life in long-run wealth accumulation. Buy term and invest the difference is a well-established strategy. Whole life makes sense only in specific estate planning scenarios.

Mistake 5: Not Reviewing Coverage After Major Life Events

Why it happens: People buy coverage, file it away, and forget. What to do instead: Review both policies after every major life event — marriage, divorce, birth, death of a beneficiary, new mortgage, job change. Your health plan network may no longer include your doctor. Your life insurance coverage amount may be insufficient for your current mortgage. Annual review takes 30 minutes and prevents costly gaps.

⚠️ WARNING: Having Life Insurance But No Health Insurance

What happens: You protect your family’s future but leave yourself financially exposed today. A $45,000 hospital bill for an uninsured surgery arrives. You drain your savings, take on medical debt at 24% APR, or decline treatment. The irony: medical bills are a leading cause of bankruptcy in the US. If you survive a serious illness uninsured, you may impoverish the family you were protecting with your life insurance. What to do instead: Always prioritise health insurance first. Then add life insurance. If you can only afford one, health insurance protects your finances today — life insurance protects your family only after you die.

Do I Need Both Life Insurance and Health Insurance?

| Your Situation | Our Recommendation |

| Single adult, no dependants, employed | ✅ Health insurance essential. Life insurance optional. |

| Married, both employed, no children | ✅ Both recommended — spouse may depend on your income even without children |

| Married with children and a mortgage | ✅ Both non-negotiable — health covers treatment; life protects the family financially |

| Self-employed, no employer plan | ✅ Health insurance critical — ACA marketplace plan immediately. Add term life if dependants exist. |

| Single parent with children | ✅ Both essential — children depend on your health AND your income |

| Retired, Medicare-eligible (65+) | ✅ Medicare covers health. Life insurance review — may no longer be needed if no dependants or mortgage. |

| Business owner with employees or partners | ✅ Both — plus consider key person life insurance and group health plan for employees |

| Young adult under 26 on parent’s health plan | ✅ Stay on parent’s health plan (ACA allows to age 26). Add term life when you have your own dependants. |

💡 Tip: The simple rule — if anyone depends on your income, you need life insurance. If you use any healthcare at all, you need health insurance. For most working adults with families, both are non-negotiable and both are more affordable than most people think: $55/month buys $500,000 of life insurance. Health insurance averages $210/month through an employer plan.

Cost Comparison: Life Insurance vs Health Insurance (2026)

| Age / Profile | Health Insurance Monthly | Life Insurance Monthly | Combined Monthly Cost |

| Age 25, healthy non-smoker | $280 (Silver individual ACA) | $18 (term life $500k 20yr, NerdWallet 2026) | $298/month total |

| Age 30, healthy non-smoker | $320 (Silver individual ACA) | $22 (term life $500k 20yr) | $342/month total |

| Age 40, healthy non-smoker | $752 (Silver ACA, Venteur 2026) | $55 (term life $500k 20yr, MoneyGeek 2026) | $807/month total |

| Age 40, smoker | $752 (Silver ACA — tobacco surcharge applies in most states) | $150–$200 (term life — smoker rates) | $950–$1,000/month total |

| Age 50, healthy non-smoker | $1,050 (Silver ACA estimate) | $120 (term life $500k 20yr) | $1,170/month total |

| Age 40, whole life ($500k) | $752 (Silver ACA) | $667 (whole life, MoneyGeek 2026) | $1,419/month total |

| UK — age 40 (term life + private health) | £45–£90 AXA Health (private) | £25–£40 term life £500k | £70–£130/month combined |

Best Providers: Life Insurance and Health Insurance (2026)

Haven Life (US) — Best Term Life Insurance

Why recommended: Fully online application; competitive term rates; backed by MassMutual (A++ AM Best). Average 40-year-old pays $55–$62/month for $500,000 20-year term. Best for: Healthy adults under 50 wanting fast, affordable term life. Rating: A++ AM Best (MassMutual backing); 4.4/5 NerdWallet.

Blue Cross Blue Shield (US) — Best Health Insurance

Why recommended: Broadest US network — 96% of hospitals and physicians; available all 50 states; strong individual and family plan options. Average individual Silver: $680–$780/month. Best for: Adults needing reliable nationwide health coverage. Rating: A+ AM Best; 3.9/5 JD Power 2025.

Legal & General (UK) — Best UK Term Life

Why recommended: UK’s largest term life insurer by market share; competitive rates from £14/month for £250,000 coverage (age 30, non-smoker, 25-year term). Best for: UK adults with mortgages needing straightforward term life protection. Rating: AA- Standard & Poor’s; 4.2/5 Trustpilot.

Bupa (UK) — Best UK Private Health Insurance

Why recommended: Comprehensive private health plans from £45–£90/month individual; fast specialist access; dental and mental health add-ons available. Best for: UK professionals wanting private healthcare alongside NHS. Rating: Defaqto 5 stars; 4.0/5 Trustpilot.

We recommend Haven Life (US) and Legal & General (UK) for term life insurance, and Blue Cross Blue Shield (US) and Bupa (UK) for health insurance. Most adults should hold both simultaneously — they serve entirely different financial needs.

Frequently Asked Questions

Do I need both life insurance and health insurance?

Yes, for most working adults with dependants. Health insurance pays for medical treatment while you are alive. Life insurance pays your family when you die. One does not substitute for the other. If you have a spouse, children, or a mortgage, both are financially essential. The combined cost is often less than most people expect: an employer health plan averages $210/month in employee contributions, and a $500,000 term life policy for a healthy 40-year-old costs just $55/month (MoneyGeek 2026).

What is the main difference between life insurance and health insurance?

Health insurance pays for your medical care while you are alive — doctor visits, hospital stays, prescriptions, and surgery. Life insurance pays a lump sum to your named beneficiaries after you die. Health insurance benefits you directly. Life insurance benefits the people who depend on you financially. They cover entirely different risks and both are necessary for comprehensive financial protection.

Is life insurance cheaper than health insurance?

Yes, significantly. A healthy 40-year-old pays an average of $55/month for $500,000 of 20-year term life insurance (MoneyGeek 2026). The same person pays an average of $752/month for an ACA Silver health plan (Venteur 2026). Health insurance is dramatically more expensive because it is used frequently throughout your lifetime, while life insurance pays out only once. Whole life insurance — at $667/month for $500,000 coverage — approaches health insurance costs, which is one reason term life is recommended for most people.

Can life insurance pay for medical bills?

No. Standard life insurance pays only a death benefit — a lump sum to beneficiaries after the policyholder dies. It does not pay medical bills while you are alive. Some life insurance policies include a terminal illness rider or accelerated death benefit rider, which can pay a portion of the death benefit early if you are diagnosed with a terminal illness (typically defined as less than 12–24 months to live). This partial early payout can help with end-of-life medical costs, but it is not a substitute for health insurance.

What happens to my health insurance if I die?

Your health insurance policy terminates immediately upon your death. It cannot be transferred to beneficiaries and pays no death benefit. Your dependants who were covered under your family health plan lose their coverage when you die and must enrol in their own plans within 60 days (qualifying life event). This is exactly why life insurance is essential — it gives your family the financial resources to pay for their own health coverage and living expenses after your death.

Does life insurance cover critical illness?

Standard term and whole life insurance does not cover critical illness — they pay only the death benefit. Critical illness insurance is a separate product that pays a lump sum if you are diagnosed with a specified serious condition (cancer, heart attack, stroke) while alive. If you want living benefits for serious illness, consider adding a critical illness rider to your life insurance or buying a standalone critical illness policy. This is distinct from both standard life insurance and health insurance.

Which should I get first — life insurance or health insurance?

Health insurance first, always. One uninsured medical event can cost $15,000–$50,000 and create financial devastation immediately. Life insurance becomes essential when you have dependants — a spouse, children, or anyone who relies on your income. If you are young and single with no dependants, health insurance is the non-negotiable priority. Add term life insurance as soon as you have anyone depending on your income. Buying both simultaneously — as employer plans allow — is the optimal approach.

Can I get life insurance without health insurance?

Yes, legally. You can buy life insurance without having health insurance. Life insurers assess your health at application (medical underwriting) but do not require you to carry ongoing health insurance. However, declining health insurance to fund life insurance premiums is financially irrational — health insurance protects you financially while you are alive; life insurance protects your family after you die. Both risks exist simultaneously and both need to be covered.

Is life insurance tax-free in the UK and US?

Yes, in most cases. In the US, life insurance death benefits are paid tax-free to beneficiaries under federal law. In the UK, the death benefit itself is not subject to income tax or capital gains tax, but it may be subject to inheritance tax (IHT) if the policy is not written in trust. UK policyholders should place their life insurance policy in trust to keep the payout outside their estate for IHT purposes — a free legal step arranged by most UK life insurers at point of sale.

What is the right amount of life insurance coverage?

The standard guideline is 10–12 times your annual income. A person earning £50,000/$70,000 per year should carry £500,000/$700,000–£840,000 of life cover. More specifically: calculate your outstanding mortgage + outstanding debts + future education costs for children + 5–10 years of family living expenses. That total is your minimum coverage requirement. For Daniel from our scenario: $800,000 mortgage + $300,000 family costs = $1,100,000 minimum coverage. He holds $1,000,000 — close enough and affordable at $28/month for a 30-year term.

Key Takeaways

- Health insurance pays for medical care while you are alive — it covers doctor visits, hospital stays, prescriptions, and surgery with a capped out-of-pocket maximum of $9,450/year (CMS 2026).

- Life insurance pays a lump sum to your beneficiaries when you die — it replaces income, clears the mortgage, and funds your family’s future without any benefit to you while alive.

- They cover entirely different risks. One does not substitute for the other. Most working adults with dependants need both simultaneously.

- Cost comparison 2026: health insurance averages $752/month for a 40-year-old (ACA Silver, Venteur 2026); term life averages $55/month for $500,000 over 20 years for the same person (MoneyGeek 2026).

- Prioritise health insurance first — one uninsured medical event can cost $15,000–$50,000+. Add term life insurance as soon as you have dependants.

- Whole life costs $667/month vs $55/month for term for the same $500,000 coverage (MoneyGeek 2026). For most people, term life + investing the difference is the better financial strategy.

- Compare term life vs whole life insurance in detail [INTERNAL LINK: term life insurance vs whole life insurance — costs benefits and which to choose in 2026]

- See how health insurance plan types affect your total annual cost [INTERNAL LINK: HMO vs PPO health insurance plans — which saves you more in 2026]

This guide reflects the latest 2026 insurance data from MoneyGeek, Venteur, and CMS.

Disclaimer

This article is for informational purposes only. Always consult a licensed insurance professional before making coverage decisions. Trust My Policy does not sell insurance products or represent any insurer.