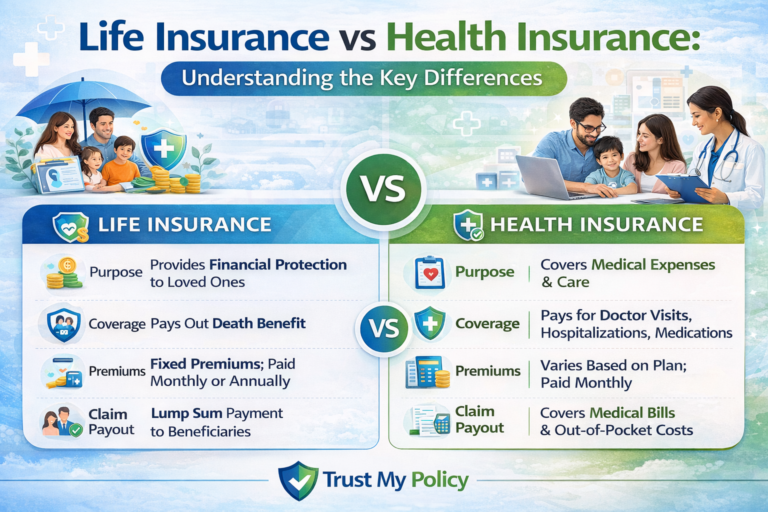

Health Insurance Coverage Explained: A Complete Guide to Understanding Your Benefits

Health insurance can be confusing for many people. Policies often include complex terms such as premiums, deductibles, copayments, and coverage limits. Without understanding these concepts, it can be difficult to know what medical services are actually covered and how much you may need to pay.

This is why health insurance coverage explained in simple terms is important for individuals and families worldwide. Health insurance coverage determines which medical services an insurance plan pays for, how much it pays, and when you are responsible for costs.

Healthcare expenses can be unpredictable. A routine doctor visit may cost a small amount, but hospital treatments, surgeries, or long-term medical care can become very expensive. Health insurance helps reduce these financial risks by sharing the cost between the insured person and the insurance provider.

However, not all health insurance policies provide the same coverage. Some plans focus on basic services, while others include broader benefits such as specialist care, preventive services, and prescription drugs.

In this guide, you will learn how health insurance coverage works, the key components of a policy, common coverage types, and how different plans compare. Understanding these details can help you make informed decisions about healthcare protection.

Health Insurance Coverage Components

| Coverage Component | What It Means | Who Pays | Why It Matters |

|---|---|---|---|

| Premium | Monthly payment to keep insurance active | Policyholder | Maintains coverage |

| Deductible | Amount paid before insurance starts covering costs | Policyholder | Determines initial expenses |

| Copayment | Fixed fee for specific services | Shared | Helps manage smaller costs |

| Coinsurance | Percentage of cost shared after deductible | Shared | Splits major expenses |

| Out-of-Pocket Maximum | Maximum yearly cost paid by the insured | Policyholder limit | Protects against large bills |

| Covered Services | Medical services included in the policy | Insurer and policyholder | Defines healthcare access |

, benefits, and financial protection options available to policyholders. Many readers compare multiple guides before selecting a plan so they can clearly evaluate premiums, claim procedures, and long‑term advantages. A useful resource to explore is Copay vs Coinsurance, which explains how this insurance policy works, the key benefits it offers, and situations where it may be the most suitable option. By reviewing this guide, you can gain deeper insights into coverage features, eligibility requirements, and practical tips that help individuals and families make smarter insurance decisions.

What Is Health Insurance Coverage?

Health insurance coverage refers to the range of medical services and costs that an insurance policy agrees to pay for or partially cover.

Coverage determines:

-

Which healthcare services are included

-

How much the insurance company will pay

-

How much the policyholder must pay

-

When coverage begins

Typical services included in health insurance coverage may include:

-

Doctor visits

-

Hospital care

-

Emergency treatment

-

Prescription medications

-

Preventive healthcare

However, each policy defines its own coverage limits and exclusions.

Key Elements of Health Insurance Coverage

Understanding the core elements of health insurance coverage helps clarify how policies work.

Premium

The premium is the regular payment required to keep an insurance policy active.

Key Characteristics

-

Usually paid monthly

-

Required regardless of healthcare usage

-

Varies based on age, location, and plan type

Example

If a health insurance plan has a $200 monthly premium, the policyholder must pay $200 every month to maintain coverage.

Deductible

The deductible is the amount a person must pay out of pocket before the insurance provider starts covering medical costs.

Key Characteristics

-

Reset each policy year

-

Can range from low to very high amounts

-

Higher deductibles often mean lower premiums

Example

If your deductible is $1,500, you must pay the first $1,500 of medical expenses before the insurance company begins contributing.

Copayment

A copayment, often called a copay, is a fixed amount paid for specific medical services.

Examples

-

Doctor visit copay: $25

-

Prescription medication copay: $10

-

Specialist visit copay: $50

Copayments help share the cost of healthcare between the patient and the insurance provider.

Coinsurance

Coinsurance is the percentage of medical costs shared between the insurance company and the policyholder after the deductible has been met.

Example

If a policy has 20% coinsurance:

-

Insurance company pays 80%

-

Policyholder pays 20%

Coinsurance applies until the out-of-pocket maximum is reached.

Out-of-Pocket Maximum

The out-of-pocket maximum is the maximum amount a person must pay for covered services within a policy year.

Once this limit is reached:

-

The insurance company typically pays 100% of covered medical expenses.

Why It Matters

This limit protects individuals from extremely high healthcare costs.

Covered Medical Services

Covered services are the medical treatments and healthcare services included in a health insurance policy.

Common covered services include:

-

Preventive care

-

Hospitalization

-

Emergency services

-

Laboratory tests

-

Prescription medications

Policies may also include additional benefits such as mental health support or maternity care.

, benefits, and financial protection options available to policyholders. Many readers compare multiple guides before selecting a plan so they can clearly evaluate premiums, claim procedures, and long‑term advantages. A useful resource to explore is Health Insurance Claim Process, which explains how this insurance policy works, the key benefits it offers, and situations where it may be the most suitable option. By reviewing this guide, you can gain deeper insights into coverage features, eligibility requirements, and practical tips that help individuals and families make smarter insurance decisions.

Common Types of Health Insurance Coverage

Health insurance plans may offer different types of coverage depending on the policy structure.

Preventive Care Coverage

Preventive care focuses on maintaining health and detecting diseases early.

Examples include:

-

Vaccinations

-

Health screenings

-

Routine checkups

-

Blood pressure tests

Preventive care can help reduce long-term healthcare costs.

Hospital and Emergency Coverage

Hospital coverage helps pay for:

-

Inpatient hospital stays

-

Surgeries

-

Emergency room visits

-

Intensive care treatment

Emergency coverage is one of the most important parts of health insurance.

Prescription Drug Coverage

Many health insurance plans include prescription drug benefits.

Coverage may vary depending on:

-

Type of medication

-

Generic vs. brand-name drugs

-

Policy drug lists

Prescription coverage can significantly reduce medication costs.

Specialist and Diagnostic Coverage

Specialist coverage includes consultations with medical professionals such as:

-

Cardiologists

-

Dermatologists

-

Orthopedic doctors

Diagnostic services may include:

-

X-rays

-

MRI scans

-

Blood tests

Some plans require referrals before visiting specialists.

Maternity and Newborn Coverage

Certain health insurance policies include maternity benefits.

These may cover:

-

Prenatal checkups

-

Delivery costs

-

Postnatal care

-

Newborn medical services

Coverage varies widely between plans and regions.

Detailed Comparison of Health Insurance Coverage Components

| Component | What It Covers | When You Pay | Impact on Total Cost |

|---|---|---|---|

| Premium | Maintains insurance policy | Monthly | Predictable expense |

| Deductible | Initial medical costs | Before insurance coverage begins | Higher deductible lowers premium |

| Copayment | Fixed service fees | During healthcare visits | Small predictable payments |

| Coinsurance | Shared treatment costs | After deductible | Percentage-based cost sharing |

| Out-of-Pocket Maximum | Annual cost protection | Throughout policy year | Prevents extreme expenses |

| Covered Services | Medical treatments included | Based on plan rules | Determines healthcare access |

Pros and Cons of Health Insurance Coverage

Pros

Financial Protection

Health insurance helps protect individuals from high medical bills.

Access to Healthcare

Insurance allows easier access to hospitals, doctors, and treatments.

Preventive Services

Many policies include screenings and vaccinations.

Cost Sharing

Insurance spreads medical costs between the individual and the insurer.

Emergency Support

Coverage ensures financial help during unexpected health emergencies.

Cons

Monthly Premium Costs

Even when no healthcare services are used, premiums must still be paid.

Deductibles and Copayments

Policyholders may still pay part of medical expenses.

Coverage Limitations

Some treatments may not be covered by certain plans.

Network Restrictions

Some policies only cover services from specific healthcare providers.

, benefits, and financial protection options available to policyholders. Many readers compare multiple guides before selecting a plan so they can clearly evaluate premiums, claim procedures, and long‑term advantages. A useful resource to explore is Renters vs Homeowners Insurance, which explains how this insurance policy works, the key benefits it offers, and situations where it may be the most suitable option. By reviewing this guide, you can gain deeper insights into coverage features, eligibility requirements, and practical tips that help individuals and families make smarter insurance decisions.

Real-Life Examples of Health Insurance Coverage

Example 1: Routine Doctor Visit

A patient visits a doctor for a regular checkup.

Costs may include:

-

$30 copayment

-

Insurance covers the rest of the consultation cost.

Example 2: Hospital Surgery

A patient requires surgery costing $10,000.

If the patient has:

-

$1,000 deductible

-

20% coinsurance

The patient may pay:

-

$1,000 deductible

-

20% of remaining cost until out-of-pocket maximum is reached.

Example 3: Preventive Screening

A preventive health screening may be fully covered by insurance without additional payment, depending on the plan.

Example 4: Prescription Medication

A patient receives medication with a $15 copay.

Insurance covers the rest of the drug cost.

Common Mistakes About Health Insurance Coverage

Many people misunderstand how health insurance coverage works.

Confusing Premiums With Total Costs

Premiums are only one part of healthcare expenses.

Other costs may include deductibles, copayments, and coinsurance.

Ignoring Coverage Limits

Some policies limit coverage for specific treatments.

Always review coverage details carefully.

Not Understanding Network Restrictions

Certain plans require patients to use approved hospitals and doctors.

Skipping Preventive Care

Preventive services help detect health problems early and may be included in many plans.

Assuming All Treatments Are Covered

Some procedures, medications, or treatments may be excluded.

Frequently Asked Questions (FAQs)

What does health insurance coverage mean?

Health insurance coverage refers to the medical services and expenses that an insurance policy agrees to pay for or help pay for.

What is the difference between deductible and copayment?

A deductible is the amount paid before insurance begins covering costs, while a copayment is a fixed fee paid when receiving specific medical services.

What is coinsurance in health insurance?

Coinsurance is the percentage of medical costs shared between the policyholder and the insurance company after the deductible is met.

What is an out-of-pocket maximum?

It is the maximum amount a person must pay for covered healthcare services in a year before insurance covers the rest.

Are preventive services included in health insurance?

Many health insurance plans include preventive services such as checkups, screenings, and vaccinations.

Does health insurance cover all medical treatments?

No. Each policy has specific inclusions and exclusions, so some treatments may not be covered.

Why is health insurance coverage important?

Health insurance helps reduce financial risks from medical expenses and provides access to healthcare services.

, benefits, and financial protection options available to policyholders. Many readers compare multiple guides before selecting a plan so they can clearly evaluate premiums, claim procedures, and long‑term advantages. A useful resource to explore is Health Insurance Without Employer, which explains how this insurance policy works, the key benefits it offers, and situations where it may be the most suitable option. By reviewing this guide, you can gain deeper insights into coverage features, eligibility requirements, and practical tips that help individuals and families make smarter insurance decisions.

Conclusion

Understanding health insurance coverage explained clearly helps individuals make better decisions about their healthcare protection.

Health insurance coverage includes several important components, such as:

-

Premiums

-

Deductibles

-

Copayments

-

Coinsurance

-

Out-of-pocket maximums

-

Covered medical services

These elements determine how medical costs are shared between the policyholder and the insurance provider.

Different health insurance plans offer varying levels of coverage, ranging from basic emergency protection to comprehensive healthcare services. Knowing what a policy includes—and what it does not include—can help avoid unexpected medical expenses.

Before choosing a health insurance plan, it is important to carefully review coverage details, compare policy structures, and understand the total potential costs.

A clear understanding of health insurance coverage allows individuals and families to select policies that provide both financial protection and access to essential healthcare services.

Disclaimer:

“Disclaimer: This article is for educational purposes only. Trust My Policy is an independent informational platform and does not sell insurance products or represent any insurance provider. Readers should consult official policy documents or licensed professionals for personalized advice.”