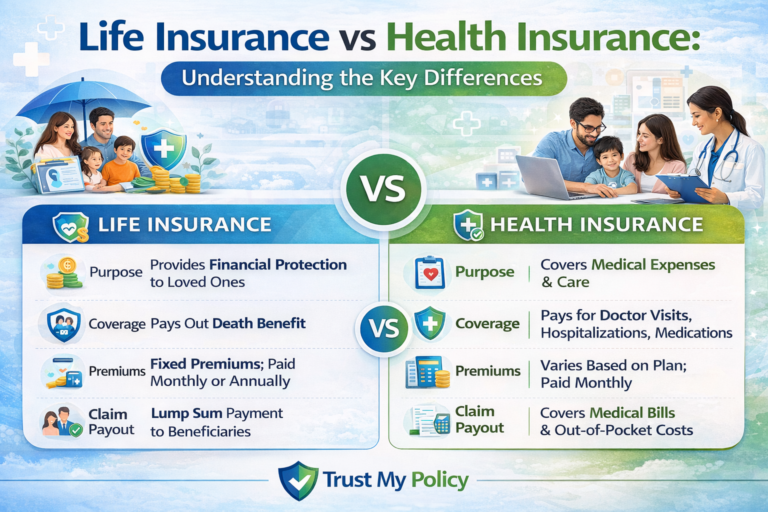

Cheap Health Insurance Options: A Complete Guide to Affordable Coverage

Health care costs continue to rise in many parts of the world. A simple hospital visit, prescription medication, or emergency treatment can become very expensive without insurance coverage. For individuals, families, students, freelancers, and retirees, finding cheap health insurance options is often a top priority.

Affordable health insurance does not always mean poor coverage. Many low-cost plans provide essential protection for major medical expenses. The key is understanding how different types of insurance work and choosing the option that matches your budget and healthcare needs.

This guide explains the most common affordable health insurance plans, how they compare, and who they are best suited for. You will also learn the advantages, disadvantages, and common mistakes people make when choosing cheaper coverage.

Whether you are self-employed, unemployed, or simply looking for a more affordable plan, understanding the available options can help you make a smarter decision and avoid unexpected medical bills.

Table of Contents

ToggleCheap Health Insurance Options

| Insurance Option | Typical Monthly Cost | Best For | Coverage Level | Flexibility |

|---|---|---|---|---|

| Government Subsidized Plans | Low to moderate | Low-income individuals | Medium to high | Moderate |

| High Deductible Health Plans (HDHP) | Low | Healthy individuals | Medium | High |

| Catastrophic Health Insurance | Very low | Young adults | Low (major emergencies) | Moderate |

| Short-Term Health Insurance | Low | Temporary coverage needs | Low to medium | High |

| Community or Cooperative Health Plans | Low | Community groups | Medium | Moderate |

| Basic Private Health Plans | Moderate | Individuals needing basic coverage | Medium | High |

This overview highlights the most common ways people lower health insurance costs while still maintaining financial protection.

, benefits, and financial protection options available to policyholders. Many readers compare multiple guides before selecting a plan so they can clearly evaluate premiums, claim procedures, and long‑term advantages. A useful resource to explore is Private Health Insurance Explained, which explains how this insurance policy works, the key benefits it offers, and situations where it may be the most suitable option. By reviewing this guide, you can gain deeper insights into coverage features, eligibility requirements, and practical tips that help individuals and families make smarter insurance decisions.

Understanding Cheap Health Insurance Options

Cheap health insurance usually means lower monthly premiums. However, these plans may have higher deductibles, limited provider networks, or fewer benefits.

Affordable insurance plans often reduce cost by:

-

Increasing deductibles

-

Limiting coverage to essential services

-

Restricting hospital or doctor networks

-

Offering government subsidies

-

Providing temporary or emergency-only protection

Understanding these trade-offs is important before selecting a plan.

Government Subsidized Health Insurance

Government-supported health insurance programs are designed to help individuals and families who cannot afford full-price insurance.

Key Features

-

Reduced premiums based on income

-

Basic healthcare services included

-

Preventive care often covered

-

Subsidies or tax credits may apply

Who Benefits Most

These plans are helpful for:

-

Low-income families

-

Unemployed individuals

-

Part-time workers

-

Students

-

Retirees without employer coverage

Typical Coverage

Government subsidized programs often include:

-

Doctor visits

-

Hospitalization

-

Preventive care

-

Prescription medications

-

Maternity services

However, coverage levels vary widely between countries.

High Deductible Health Plans (HDHP)

High Deductible Health Plans are a common cheap health insurance option. These plans reduce monthly premiums but require you to pay more out-of-pocket before coverage begins.

How HDHP Works

A deductible is the amount you must pay before insurance starts covering expenses.

For example:

-

Deductible: $3,000

-

Insurance pays after deductible is met

Because you pay more upfront, the monthly premium is lower.

Key Characteristics

-

Lower monthly premium

-

Higher deductible

-

Preventive care often covered early

-

Emergency coverage included

Best For

HDHP plans are often suitable for:

-

Healthy individuals

-

Young adults

-

People who rarely visit doctors

-

Freelancers or gig workers

, benefits, and financial protection options available to policyholders. Many readers compare multiple guides before selecting a plan so they can clearly evaluate premiums, claim procedures, and long‑term advantages. A useful resource to explore is Short Term Health Insurance Explained, which explains how this insurance policy works, the key benefits it offers, and situations where it may be the most suitable option. By reviewing this guide, you can gain deeper insights into coverage features, eligibility requirements, and practical tips that help individuals and families make smarter insurance decisions.

Catastrophic Health Insurance

Catastrophic plans focus only on major medical emergencies.

These plans offer extremely low premiums but limited routine coverage.

What Catastrophic Plans Cover

Typically includes:

-

Emergency hospital care

-

Surgery

-

Major illnesses

-

Life-threatening accidents

Routine services like doctor visits may not be covered until the deductible is met.

Why They Are Affordable

Costs are low because:

-

Coverage activates only after large expenses

-

Limited routine benefits

-

Higher deductibles

Ideal Users

Catastrophic insurance works best for:

-

Young adults

-

People under 30 in some countries

-

Healthy individuals

-

Those needing financial protection against major emergencies

Short-Term Health Insurance

Short-term plans provide temporary coverage for a limited period, often between 3 months and 12 months.

These plans are often used during life transitions.

Common Situations for Short-Term Plans

People use short-term insurance when:

-

Changing jobs

-

Waiting for new insurance to begin

-

Recently graduating

-

Temporarily unemployed

-

Relocating to another country

Coverage Characteristics

Short-term policies may include:

-

Emergency medical treatment

-

Hospital care

-

Limited doctor visits

-

Some prescription coverage

However, they usually exclude:

-

Pre-existing conditions

-

Maternity services

-

Mental health care

, benefits, and financial protection options available to policyholders. Many readers compare multiple guides before selecting a plan so they can clearly evaluate premiums, claim procedures, and long‑term advantages. A useful resource to explore is Types of Insurance Explained, which explains how this insurance policy works, the key benefits it offers, and situations where it may be the most suitable option. By reviewing this guide, you can gain deeper insights into coverage features, eligibility requirements, and practical tips that help individuals and families make smarter insurance decisions.

Community or Cooperative Health Plans

Community health insurance pools resources from members of a group or cooperative.

Members share risks and healthcare costs collectively.

How These Plans Work

Participants pay a regular fee into a community fund. The fund helps cover medical expenses for members.

Advantages

These programs often:

-

Lower costs through shared risk

-

Offer local medical support

-

Focus on preventive care

Common Examples

These plans may be offered through:

-

Community organizations

-

Worker associations

-

Agricultural cooperatives

-

Nonprofit healthcare programs

Availability varies depending on the region.

Basic Private Health Insurance Plans

Basic private plans offer limited but essential healthcare coverage at a relatively affordable cost.

These plans typically include:

-

General practitioner visits

-

Basic hospitalization

-

Essential diagnostics

-

Emergency services

They usually exclude advanced treatments, elective procedures, or premium hospital networks.

Basic plans are often used by:

-

Freelancers

-

Small business owners

-

Self-employed professionals

-

Individuals without employer coverage

Detailed Comparison of Cheap Health Insurance Options

| Feature | Government Subsidized | HDHP | Catastrophic | Short-Term | Community Plans | Basic Private |

|---|---|---|---|---|---|---|

| Monthly Premium | Low | Low | Very low | Low | Low | Moderate |

| Deductible | Low to moderate | High | Very high | Moderate | Low | Moderate |

| Preventive Care | Often included | Often included | Limited | Limited | Usually included | Basic coverage |

| Emergency Coverage | Yes | Yes | Yes | Yes | Yes | Yes |

| Coverage Duration | Long term | Long term | Long term | Temporary | Long term | Long term |

| Pre-existing Conditions | Usually covered | Covered after deductible | Often excluded | Often excluded | Usually covered | May vary |

| Flexibility | Moderate | High | Moderate | High | Moderate | High |

This comparison shows how different insurance structures reduce costs in different ways.

Pros and Cons of Cheap Health Insurance Options

Pros

-

Lower monthly premiums

-

Basic financial protection

-

Access to essential healthcare

-

Prevents large medical debt

-

Flexible options for different situations

-

Good for young or healthy individuals

Cons

-

Higher deductibles

-

Limited provider networks

-

Restricted benefits

-

Possible exclusions

-

Higher out-of-pocket expenses

Understanding both sides helps people choose wisely.

, benefits, and financial protection options available to policyholders. Many readers compare multiple guides before selecting a plan so they can clearly evaluate premiums, claim procedures, and long‑term advantages. A useful resource to explore is Insurance for Consultants, which explains how this insurance policy works, the key benefits it offers, and situations where it may be the most suitable option. By reviewing this guide, you can gain deeper insights into coverage features, eligibility requirements, and practical tips that help individuals and families make smarter insurance decisions.

Real-Life Use Cases

Example 1: Freelancers and Gig Workers

Independent workers often lack employer health insurance.

Many choose:

-

High Deductible Health Plans

-

Basic private insurance

-

Government subsidy programs

These options keep premiums manageable while providing emergency protection.

Example 2: Young Adults Starting Careers

Young professionals often select:

-

Catastrophic plans

-

High deductible plans

Because they generally use healthcare less frequently, these plans help reduce monthly costs.

Example 3: Temporary Job Transitions

Someone leaving one job and waiting to start another may use:

-

Short-term health insurance

This prevents a coverage gap during the transition period.

Example 4: Rural Communities

Some rural areas use community health insurance programs.

Local groups pool funds and support members during illness or emergencies.

This model is common in developing regions.

Common Mistakes When Choosing Cheap Health Insurance

Choosing the cheapest plan without understanding the details can lead to problems.

1. Ignoring Deductibles

A low premium may hide a very high deductible. This means large out-of-pocket expenses before coverage begins.

2. Not Checking Network Hospitals

Some plans limit which hospitals or doctors you can visit.

Always verify the provider network.

3. Overlooking Coverage Limits

Some policies cap annual benefits.

This can become risky during serious illness.

4. Ignoring Exclusions

Cheap plans sometimes exclude:

-

Pre-existing conditions

-

Maternity care

-

Mental health services

Always review policy exclusions carefully.

5. Choosing Temporary Plans for Long-Term Needs

Short-term plans may not provide comprehensive coverage and are not suitable for long-term healthcare protection.

Frequently Asked Questions (FAQs)

What is the cheapest type of health insurance?

Catastrophic health insurance and high deductible plans usually have the lowest monthly premiums.

However, they often come with higher deductibles and limited benefits.

Is cheap health insurance worth it?

Affordable insurance can still provide valuable protection against expensive medical emergencies.

The key is choosing a plan that balances cost with necessary coverage.

Can cheap insurance cover major hospital bills?

Many low-cost plans still include emergency and hospitalization coverage, but deductibles and limits may apply.

Always review policy details carefully.

Who should consider high deductible health plans?

These plans are often suitable for:

-

Healthy individuals

-

Young adults

-

People with low medical expenses

They help reduce monthly premiums while maintaining protection for major medical events.

Are short-term health insurance plans reliable?

Short-term plans can be useful for temporary coverage gaps. However, they may not include comprehensive benefits.

They are best used for short periods rather than long-term protection.

Do cheap health insurance plans cover pre-existing conditions?

Some plans cover pre-existing conditions, especially government programs or long-term policies.

Short-term and catastrophic plans may exclude them.

Conclusion

Healthcare expenses can be unpredictable, making health insurance an important financial safeguard. While comprehensive plans offer extensive coverage, they may not fit every budget. Fortunately, several cheap health insurance options provide essential protection at lower costs.

Common affordable choices include government subsidized plans, high deductible health plans, catastrophic insurance, short-term coverage, community programs, and basic private policies. Each option lowers costs in different ways, such as higher deductibles, limited benefits, or temporary coverage.

Choosing the right plan requires balancing monthly premiums, deductibles, coverage limits, and healthcare needs. A plan that looks cheap at first may become expensive if it lacks necessary protection.

By understanding the differences between these insurance types and carefully reviewing policy details, individuals and families can find affordable coverage that protects both their health and their finances.

Disclaimer:

“Disclaimer: This article is for educational purposes only. Trust My Policy is an independent informational platform and does not sell insurance products or represent any insurance provider. Readers should consult official policy documents or licensed professionals for personalized advice.”