Life Insurance Payout: How It Works and How to Claim 2026

A life insurance payout is the death benefit paid tax-free to nominated beneficiaries when the insured person dies while the policy is active. UK insurers typically pay within 5–30 working days of receiving all required documents. USA insurers typically pay within 30–60 days. The payout is income-tax-free in both countries. UK policies written in trust bypass probate, paying in weeks rather than months. The most common reasons for payout delays or denials: non-disclosure, lapsed policy due to missed premiums, death within exclusion period (suicide clause), or policy not written in trust causing probate delays.

When Tom’s father died unexpectedly, Tom had no idea his father even had a life insurance policy. Six months later, sorting through financial documents, he found a policy document. He called the insurer. Within 12 working days, £125,000 arrived in Tom’s bank account — tax-free. The entire process required a death certificate, the policy document, and one phone call. Tom had expected months of delay and bureaucracy. The reality was straightforward because his father had done everything right: named Tom as beneficiary, kept premiums paid, and been fully honest on the application.

A life insurance payout is the lump sum or monthly income the insurance company pays to your beneficiaries when you die. Understanding how it works — the claims process, the timelines, what can delay or deny it, and what your family needs to do — is as important as the policy itself. A policy no one can claim is worthless.

This guide explains exactly how life insurance payouts work in the UK and USA in 2026: the step-by-step claims process, average timelines, why claims are denied, what makes a claim fail, and how to ensure your family receives the payout smoothly and quickly.

Life Insurance Payout: Quick Summary

| Feature | UK | USA |

| Is the payout taxable? | Income tax free. May be subject to IHT if not written in trust (40% above £325k threshold) | Income tax free (IRC Section 101a). May be included in taxable estate. |

| Typical payment timeline | 5–30 working days after documents received | 30–60 days after claim approved |

| What documents are needed | Death certificate, policy document, beneficiary ID, completed claim form | Death certificate, policy document, beneficiary ID, claim form; medical records for large claims |

| What can delay the claim | Missing documents, non-disclosure investigation, inquest or criminal investigation | Same as UK; some states require notarised documents |

| What voids the claim | Non-disclosure, missed premiums (lapsed policy), suicide within exclusion period, fraudulent application | Same as UK |

| Does probate affect the payout? | Yes — unless policy written in trust. Probate adds 6–12 months delay | Yes — beneficiary designation on policy bypasses probate in most states |

| Who pays if insurer is insolvent? | Financial Services Compensation Scheme (FSCS) | State Guaranty Association (limits vary by state, typically $300k–$500k) |

What Is a Life Insurance Payout?

Think of a life insurance payout like a cheque written in advance. You pay premiums over many years. If you die while the policy is active, the insurer cashes that cheque and sends it to whoever you nominated. The payout arrives at the moment your family needs money most and is completely free of income tax.

The life insurance payout — also called the death benefit or sum assured — is the amount of money your insurer pays to your beneficiaries upon your death during the policy term. For term life policies, this is only paid if you die during the defined term. For whole life and permanent policies, it is paid whenever you die, as long as premiums are current.

The payout is used by most families for: Mortgage repayment or rent coverage, replacing the deceased’s income for surviving dependants, funeral and burial costs, outstanding debts and credit card balances, children’s education costs, and maintaining the family’s standard of living. There is no restriction on how the money is used — it belongs entirely to the beneficiaries.

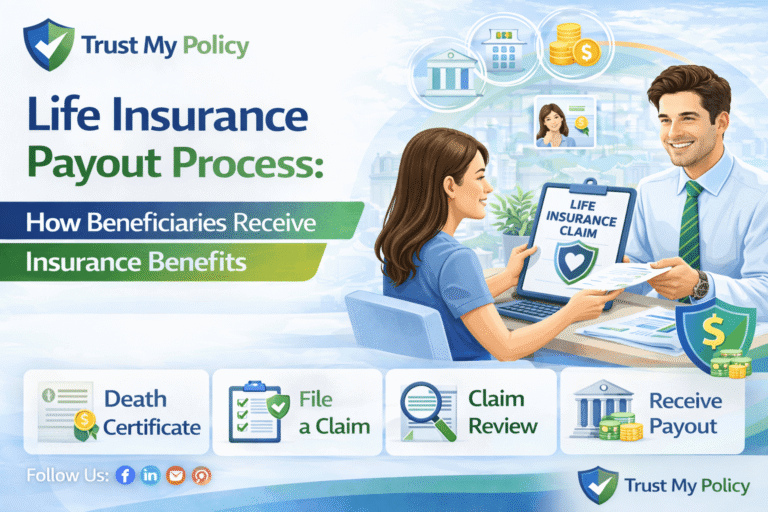

5-Step Life Insurance Claims Process

- Step 1: Notify the insurer. Contact the insurance company’s bereavement team as soon as reasonably possible after the death. Most major UK and USA insurers have dedicated 24/7 bereavement lines. You do not need to have all documents ready to make the initial notification — calling immediately starts the process.

- Step 2: Gather documents. You will typically need: the original death certificate (or certified copy), the policy schedule or policy number, proof of identity for the beneficiary (passport or driving licence), and the completed claim form provided by the insurer. For larger claims, the insurer may request GP records, a coroner’s report, or hospital records.

- Step 3: Submit the claim. Send all documents to the insurer’s claims department by post, upload them to their online portal, or deliver them via their app (some large UK and USA insurers now accept digital claim submissions). Keep copies of everything you submit.

- Step 4: The insurer investigates. The insurer verifies that the policy was in force at the time of death, premiums were paid up to date, the cause of death is not excluded by the policy, and the application was completed honestly. For straightforward claims, this takes 5–10 working days. For complex claims or those requiring medical evidence, it may take 4–8 weeks.

- Step 5: The payout is made. If approved, the insurer pays the full death benefit to the nominated beneficiary — in the UK, typically within 5–30 working days of receiving all documents. UK claims that have been written in trust are paid directly to the trustees without going through probate. USA claims are typically paid within 30–60 days.

How Long Does a Life Insurance Payout Take?

| Scenario | UK Timeline | USA Timeline |

| Straightforward claim — all documents ready, no complications | 5–15 working days | 14–30 days |

| Missing documents — claim form incomplete or death certificate delayed | Paused until documents received; then 5–15 working days | Same |

| Medical investigation required — cause of death unclear or large claim amount | 4–8 weeks additional | 4–8 weeks additional |

| Coroner’s inquest — death under investigation | Paused until inquest concludes; can take months | Same |

| Non-disclosure investigation — discrepancy between application and medical records | Can take 3–6 months or longer | Can take 3–6 months or longer |

| Policy NOT written in trust (UK) — estate goes through probate | 6–12 months additional before beneficiary receives funds | Beneficiary designation typically bypasses probate in most US states |

| 💡 TIP: Write Your UK Policy in Trust to Cut Months from the Claim Timeline

A UK life insurance policy written in trust bypasses probate entirely. The trustees can claim the payout within weeks of the death certificate arriving — without waiting for probate to be granted. Without trust, your family may wait 6–12 months for probate before accessing the funds. Writing in trust is free and takes 10 minutes at the time of policy application. It also removes the payout from your taxable estate, potentially saving 40% IHT on larger payouts. There is no reason not to do this. |

Why Life Insurance Claims Are Denied

| Reason for Denial | What It Means | How to Prevent It |

| Non-disclosure / misrepresentation | The application contained false or incomplete information about health, lifestyle, or occupation. Insurer discovers discrepancy when reviewing medical records. | Always disclose fully and accurately on the application. If circumstances change after the policy starts, notify the insurer. |

| Lapsed policy — missed premiums | Premiums were not paid, and the policy lapsed. No active policy = no claim. Most insurers offer a 30-day grace period. | Set premiums on direct debit. Contact the insurer immediately if you miss a payment — most will reinstate without penalty if resolved quickly. |

| Suicide exclusion | Most policies exclude suicide in the first 12–24 months (UK) or 2 years (USA). Death by suicide within this period results in payout of premiums only, not the full death benefit. | Buy the policy as early as possible. After the exclusion period expires, suicide is covered like any other cause. |

| Excluded activity | Death occurred during an activity explicitly excluded by the policy (e.g. extreme sport declared as excluded, aviation, warfare). Usually documented in the policy schedule. | Read the exclusions before buying. Declare all relevant activities at application — some insurers add a premium; others exclude; better to know before committing. |

| Death outside the policy term | For term life insurance, the policy has expired and the death occurs after the term end date. | This is expected — term life does not pay after the term expires. Convert to permanent coverage before term ends if continuing protection is needed. |

| Fraudulent application | The application was completed with deliberate dishonesty — age, occupation, health, or lifestyle misrepresented. | Fraud voids the policy completely. Never misrepresent information on a life insurance application. |

| ⚠️ WARNING: Non-Disclosure Is the Single Most Dangerous Application Mistake

UK and USA insurers review medical records — including GP notes and prescription history — when processing life insurance claims. Any discrepancy between what you declared on the application and what your records show gives the insurer grounds to void the policy and deny the claim. This includes conditions you knew about but thought were minor, treatments you forgot to mention, or lifestyle factors like smoking history. Being honest on the application — even if it increases your premium slightly — is always the right decision. A denied claim is infinitely more expensive than a higher premium. |

Is a Life Insurance Payout Taxable?

UK: Life insurance payouts are free of income tax and capital gains tax. However, if the policy is not written in trust, the payout forms part of your estate and may be subject to 40% inheritance tax on amounts above the £325,000 nil-rate band (plus the £175,000 Residence Nil Rate Band if applicable). Writing the policy in trust removes it from your estate entirely — making it both IHT-free and probate-free.

USA: Life insurance death benefits are generally income-tax-free to beneficiaries under IRC Section 101(a). However, if the death benefit is included in the deceased’s taxable estate, it may be subject to federal estate tax (40% above the federal exemption, currently $12.92 million per individual in 2026). Beneficiary designations on the policy itself — not a will — determine who receives the proceeds and typically bypass estate tax inclusion for most middle-income policyholders.

4 Real Life Insurance Payout Scenarios

Scenario 1: Tom’s Father — Straightforward Claim, Policy in Trust, UK

Policy in trust, beneficiary clearly named, premiums paid by direct debit, full disclosure on application. Death certificate obtained within 5 days. Claim submitted online. Payout: £125,000 within 12 working days. Zero delays. Zero IHT. Probate not needed.

Scenario 2: Karen — Claim Delayed by Non-Disclosure Investigation, UK

Karen’s husband had told his insurer he was a non-smoker on his 2019 application. His GP records showed he had smoked regularly until 2017 — which he genuinely believed was outside the typical 12-month smoking definition window. The insurer investigated for 4 months before confirming he had been smoke-free for over 12 months at application. Claim paid in full — but 4 months of waiting and stress for Karen. Lesson: Disclose everything and let the insurer make the determination.

Scenario 3: Michael’s Family — Policy Lapsed, USA

Michael had been in hospital for 3 weeks. During this time, his direct debit failed due to a bank account change. He missed two premium payments. His policy lapsed. He died 6 days after discharge. His wife filed a claim. It was denied — no active policy. Total payout: $0. Monthly premium he’d missed: $87. Lesson: Set premiums on the most reliable bank account you have. Call your insurer from the hospital if you think payments might be at risk.

Scenario 4: Estate Planning, Policy NOT in Trust — UK

David had a £300,000 whole life policy with no trust. He died with an estate of £650,000 including the £300,000 policy. His executors had to apply for probate. The process took 11 months. During this time, his family had no access to the life insurance money. On distribution, the estate was taxed at 40% on £125,000 (amount above combined nil-rate bands) = £50,000 in IHT. The £300,000 policy contributed to this taxable estate calculation. Had the policy been written in trust, it would have paid directly to the family, bypassed probate, and been excluded from the estate entirely.

Frequently Asked Questions

How long does a life insurance payout take in the UK?

UK life insurance payouts typically take 5–30 working days from receipt of all required documents. Straightforward claims with all documents ready are usually resolved in 5–15 working days. Complex claims requiring medical records, coroner reports, or non-disclosure investigations can take 3–6 months. Policies written in trust bypass probate and pay within weeks — policies not in trust may require 6–12 months of probate before the family receives anything.

How long does a life insurance payout take in the USA?

US life insurance payouts typically take 14–60 days from receipt of all required documentation. State laws in most states require insurers to pay claims within 30 days of receiving proof of death and the completed claim form. Contested claims or those requiring investigation may take 3–6 months. Beneficiary designations on the policy itself (not a will) typically bypass probate in most US states.

What do you need to claim a life insurance payout?

Standard requirements for both UK and USA claims: certified copy of the death certificate, the original policy document or policy number, completed claim form (provided by the insurer), and proof of identity for the beneficiary (passport or driving licence). Additional documents that may be requested: GP or hospital records for large claims or unusual circumstances, coroner’s report if an inquest is underway, or marriage/divorce certificates if beneficiary details have changed.

Is a life insurance payout subject to inheritance tax (UK)?

A life insurance payout is not automatically subject to inheritance tax in the UK. However, if the policy is not written in trust, the payout forms part of your estate and could be taxed at 40% on amounts above the £325,000 nil-rate band (plus £175,000 RNRB if applicable). Writing the policy in trust removes it from your estate entirely — the payout is then inheritance-tax-free and bypasses probate. This is why writing a UK policy in trust is always recommended.

Key Takeaways

- A life insurance payout is income-tax-free in both the UK and USA — beneficiaries receive the full death benefit.

- UK payouts typically arrive in 5–30 working days from receipt of all documents. USA payouts typically arrive within 30–60 days.

- Non-disclosure is the most common cause of payout denial — insurers check medical records at claim time. Always disclose fully on the application.

- Set premiums on direct debit from your most reliable bank account — a lapsed policy pays nothing.

- In the UK, write every life insurance policy in trust — it bypasses probate (saving 6–12 months), removes the payout from your taxable estate, and costs nothing to do.

- In the USA, name beneficiaries directly on the policy — this bypasses probate in most states, regardless of what your will says.

For guidance on choosing the right policy to ensure your family receives a payout, see our what is the best life insurance policy guide.

| 📋 Disclaimer

This article is for informational purposes only. Always consult a licensed insurance professional before making coverage decisions. Trust My Policy does not sell insurance products or represent any insurer. |